|

CLEAN

GROWTH STRATEGY

ABOUT -

CONTACTS - FOUNDATION -

HOME - A-Z INDEX

THERESA

MAY - Our Prime

Minister has said her government is serious about improving the environment after pressure groups gave a lukewarm response to a 25-year green plan, praising its ambition but warning that it lacked sufficient proposals for immediate action.

The

Climate Change Act 2008 (c 27) is an Act of the Parliament of

the United

Kingdom. The Act makes it the duty of the Secretary of

State to ensure that the net UK carbon account for all six

Kyoto greenhouse gases for the year 2050 is at least 80% lower

than the 1990 baseline, toward avoiding dangerous climate

change. The Act aims to enable the United Kingdom to become a low-carbon

economy and gives ministers powers to introduce the

measures necessary to achieve a range of greenhouse gas

reduction targets. An independent Committee on Climate

Change has been created under the Act to provide advice to

UK Government on these targets and related policies. In the

act Secretary of State refers to the Secretary

of State for Energy and Climate Change.

The

Climate Change Act 2008 (CCA) would mean nothing without a

Clean Growth Strategy. The following is reproduced from the

Government's website for review and comment:

UK CLEAN GROWTH STRATEGY POLICY

Clean growth means growing our national income while cutting greenhouse gas emissions1. Achieving clean growth, while ensuring an affordable energy supply for businesses and consumers, is at the heart of the UK’s Industrial Strategy. It will increase our productivity, create good jobs, boost earning power for people right across the country, and help protect the climate and environment upon which we and future generations depend.

1. UK LEADERSHIP AND PROGRESS

Our strategy for clean growth starts from a position of strength.

The UK was one of the first countries to recognise and act on the economic and security threats of climate change. The Climate Change Act, passed in 2008, committed the UK to reducing greenhouse gas emissions by at least 80% by 2050 when compared to 1990 levels, through a process of setting 5 year caps on greenhouse gas emissions termed ‘Carbon Budgets’. This approach has now been used as a model for action across the world, and is mirrored by the United Nations’ Paris Agreement.

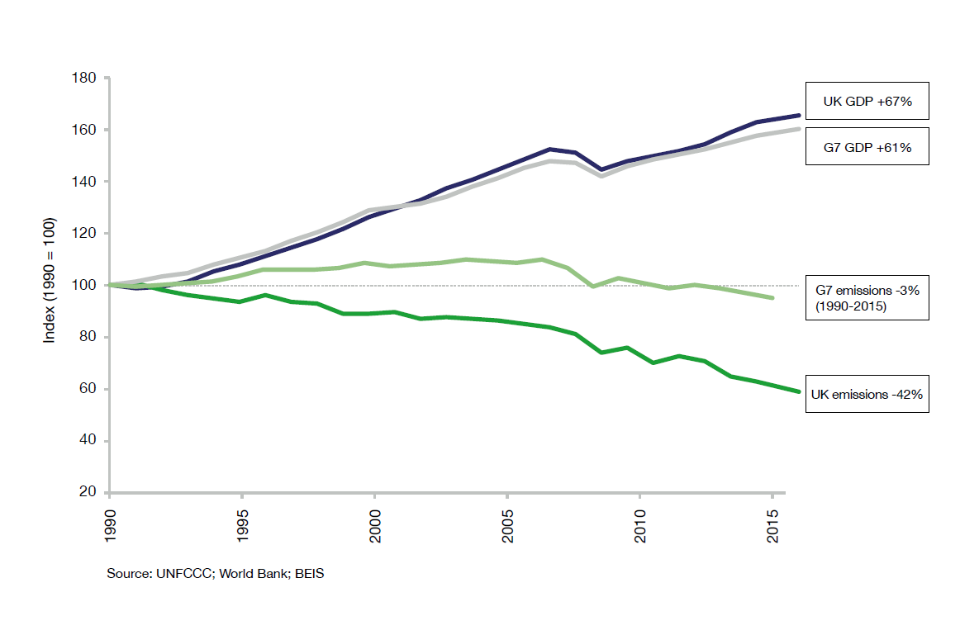

We have been among the most successful countries in the developed world in growing our economy while reducing emissions. Since 1990, we have cut emissions by 42%2 while our economy has grown by two-thirds3. This means that we have reduced emissions faster than any other G7 nation, while leading the G7 group of countries in growth in national income over this period4.

This progress has meant that we have outperformed the target emissions reductions of our first carbon budget (2008 to 2012) by 1%5 and we project that we will outperform against our second and third budgets, covering the years 2013 to 2022, by almost 5% and 4% respectively6. Our economy is expected to grow by 12% over that time7. This will be a significant achievement.

We have made progress across every sector of our economy.

1.1 Figure 1: UK and G7 economic growth and emissions

reductions (8)

In 2016, 47% of our electricity came from low carbon sources, around double the level in 20109, and we now have the largest installed offshore wind capacity in the world. Our homes and commercial buildings have become more efficient in the way they use energy which helps to reduce emissions and also cut energy bills, for example average household energy consumption has fallen by 17% since 199010. Automotive engine technology has helped drive down emissions per kilometre driven by up to 16% and driving a new car bought in 2015 will save car owners up to £200 on their annual fuel bill, compared to a car bought new in 200011. England also recycles nearly 4 times more than it did in 200012.

This progress has been aided by the falling costs of many low carbon technologies: renewable power sources like solar and wind are comparable in cost to coal and gas in many countries13; energy efficient light bulbs are over 80% cheaper today than in 201014; and the cost of electric vehicle battery packs has tumbled by over 70% in this

time (15).

As a result of this technological innovation, new high value jobs, industries and companies have been created. And this is driving a new, technologically innovative, high growth and high value ‘low carbon’ sector of the UK economy. Not only are we rapidly decarbonising parts of the domestic economy, but thanks to our world leading expertise in technologies such as offshore wind, power electronics for low carbon vehicles and electric motors, and global leadership in green finance, we are successfully exporting goods and services around the world – for example, 1 in every 5 electric vehicles driven in Europe is made in the UK16. This progress now means there are more than 430,000 jobs in low carbon businesses and their supply chains, employing people in locations right across the

country (17).

This progress has altered the way that we see many of the trade-offs between investing in low carbon technologies that help secure our future but that might incur costs today. It is clear that actions to cut our emissions can be a win-win: cutting consumer bills, driving economic growth, creating high value jobs and helping to improve our quality of life.

Of course, greenhouse gas emissions are a global problem and action is needed from all countries. The UK has played a key role in demonstrating international leadership on tackling climate change through its domestic action, climate diplomacy and financial support. The UK was among the first to recognise climate change as an economic and political issue as opposed to solely an environmental one and has used its world leading economic, science and technical skills to shape the global debate around climate change, for instance making the economic case for climate action in the landmark Stern Report in 200618. The UK has also used its influence and resources to help developing countries with their own clean growth – and our actions to date are expected to save almost 500 million tonnes of carbon dioxide over the lifetime of the projects19, more than the entire annual emissions of France20. While we do not count these results against our domestic targets, we can be proud of the impact of the UK’s commitment to global climate action.

2.

THE OPPORTUNITIES

The UK played a central role in securing the 2015 Paris Agreement in which, for the first time, 195 countries (representing over 90% of global economic

activity (21) agreed stretching national targets to keep the global temperature rise below 2 degrees. The actions and investments that will be needed to meet the Paris commitments will ensure the shift to clean growth will be at the forefront of policy and economic decisions made by governments and businesses in the coming decades. This creates enormous potential economic opportunity

– an estimated $13.5 trillion of public and private investment in the global energy sector alone will be required between 2015 and 2030 if the signatories to the Paris Agreement are to meet their national

targets (22). The decision by the US to withdraw from the Paris Agreement served to bring together and bolster action internationally on climate change with many countries underlining their commitment to the Paris Agreement in the days and weeks that followed.

The UK is well placed to take advantage of this economic opportunity. Our early action on clean growth means that we have nurtured a broad range of low carbon industries, including some sectors in which we have world leading positions. This success is built upon wider strengths – our scientific research base23, expertise in high-value service and financial industries24, and a regulatory framework that provides long-term direction and support for innovation and excellence in the design and manufacturing of leading edge technology.

Capturing part of the global opportunity while continuing to drive down carbon emissions from our own activities could provide a real national economic boost. The UK low carbon economy could grow by an estimated 11% per year between 2015 and 2030 – 4 times faster than the rest of the

economy (25) – and could deliver between £60 billion and £170 billion of export sales of goods and services by 203026. This means that clean growth can play a central part in our Industrial Strategy – building on our strengths to drive economic growth and boost earning power across the country.

Action to deliver clean growth can also have wider benefits. For example, the co-benefit of cutting transport emissions is cleaner air, which has an important effect on public health, the economy, and the environment.

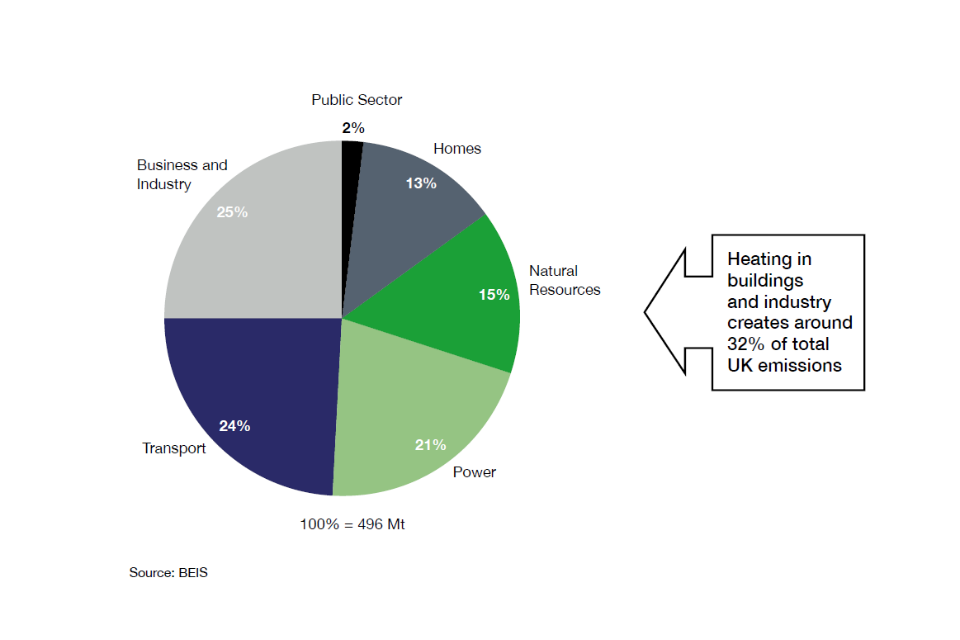

But hitting our carbon budgets and expanding the low carbon economy will not be easy. We have achieved significant results in the power and waste sectors and now need to replicate this success across the economy, particularly in the transport, business and industrial sectors. We also need to reduce the emissions created by heating our homes and businesses, which account for almost a third of UK emissions. If done in the right way, cutting emissions in these areas can benefit us all through reduced energy bills, which will help improve the UK’s productivity, and improved air quality, while the innovation and investment required to drive these emissions down can create more jobs and more export opportunities.

2.1 Figure 2: UK emissions by sector, 2015

In order to meet the fourth and fifth carbon budgets (covering the periods 2023 to 2027 and 2028 to 2032) we will need to drive a significant acceleration in the pace of decarbonisation and in this strategy we have set out stretching domestic policies that keep us on track to meet our carbon budgets. However, we are prepared to use the flexibilities available to us to meet carbon budgets, subject to the requirements set out in the Climate Change Act, if this presents better value for UK taxpayers, businesses and domestic consumers.

Every action that we take to cut emissions must be done while ensuring our economy remains competitive. As we set out in our Industrial Strategy Green Paper, we attach great importance to making sure our energy is affordable28. This is why the government has commissioned an independent review into the cost of energy led by Professor Dieter Helm

CBE. This review will recommend ways to deliver the government’s carbon targets and ensure security of supply at minimum cost to both industry and domestic consumers. Once ministers have had the opportunity to consider the review’s proposals, the government will incorporate its recommendations into the further development of the Clean Growth Strategy as appropriate.

Another imminent challenge is to manage any impact of leaving the European Union as the government fulfils its commitment to the British people. Leaving the EU will not affect our statutory commitments under our own domestic Climate Change Act and indeed our domestic binding emissions reduction targets are more ambitious than those set by EU legislation. The exact nature of the UK’s future relationship with the EU and the long-term shape of our involvement in areas like the EU Emissions Trading System are still to be determined. There are also emerging opportunities to drive more action – for example by putting emission reductions and land stewardship at the heart of a post EU agricultural support policy. We will therefore carefully examine each area of common interest with our EU partners and work to deliver policies and programmes that are at least as beneficial as the current arrangements.

3.

OUR CLEAN GROWTH STRATEGY

This strategy sets out a comprehensive set of policies and proposals that aim to accelerate the pace of ‘clean growth’, i.e. deliver increased economic growth and decreased emissions.

3.1 Our approach

In the context of the UK’s legal requirements under the Climate Change Act, the UK’s approach to reducing emissions has 2 guiding objectives:

To meet our domestic commitments at the lowest possible net cost to UK taxpayers, consumers and businesses; and,

To maximise the social and economic benefits for the UK from this transition.

In order to meet these objectives, the UK will need to nurture low carbon technologies, processes and systems that are as cheap as possible.

We need to do this for several reasons. First, we need to protect our businesses and households from high energy costs. Second, if we can develop low cost, low carbon technologies in the UK, we can secure the most industrial and economic advantage from the global transition to a low carbon economy. Third, if we want to see other countries, particularly developing countries, follow our example, we need low carbon technologies to be cheaper and to offer more value than high carbon ones.

We cannot predict every technological breakthrough that will help us meet our targets. Instead, we must create the best possible environment for the private sector to innovate and invest. Our approach will maintain that of our Industrial Strategy: building on the UK’s strengths, improving productivity across the UK and ensuring we are the best place for innovators and new business to start up and grow. We are clear about the need to design competitive markets and smart regulation to support entrepreneurs and investors who will develop the new technologies at the scale we need. This will help our wider aim of improving the UK’s earning power.

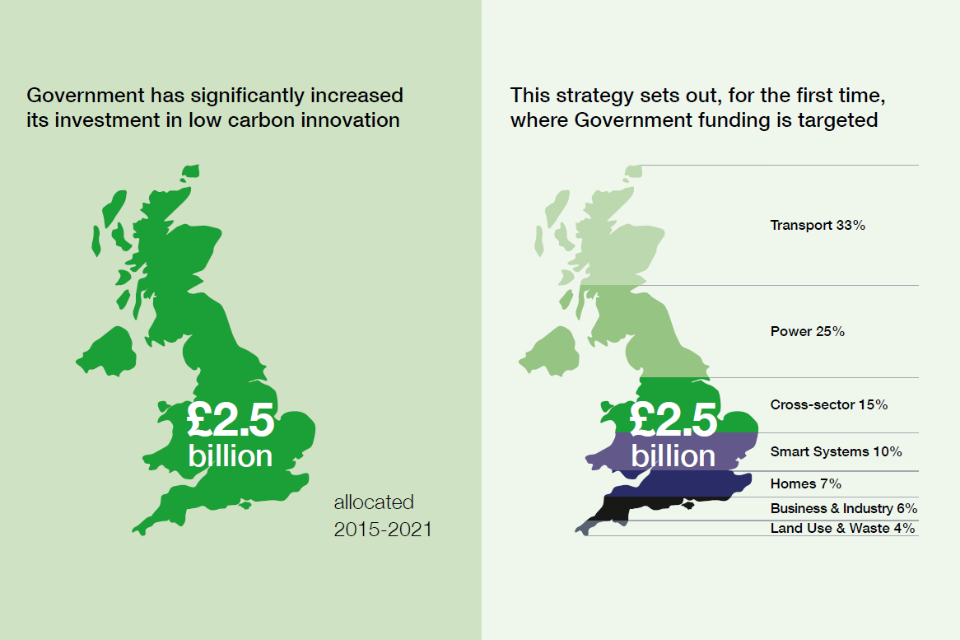

It is only through innovation – nurturing better products, processes and systems – that we will see the cost of clean technologies come down. That is why this strategy sets out for the first time how over £2.5 billion will be invested by the government to support low carbon innovation from 2015 to 2021. More broadly, the National Productivity Investment Fund will provide an additional £4.7 billion, with an extra £2 billion a year by 2020 to 2021, representing the largest increase in public spending on UK science, research and innovation since 197929. The UK is also working collaboratively as a core member of ‘Mission Innovation’30, a group of leading countries which aims to drive forward clean energy innovation on a global scale.

In addition to supporting innovation, we are focused on policies that deliver social and economic benefits beyond the imperative to reduce emissions. Higher quality, more energy efficient buildings are healthier places to live and work. Reducing the amount of heat we waste will reduce bills. Accelerating the rollout of low emission vehicles contains a triple win for the UK in terms of industrial opportunity, cleaner air and lower greenhouse gas emissions. And crucially, many of the actions in the Clean Growth Strategy will enhance the UK’s energy security by delivering a more diverse and reliable energy mix.

Actions taken by the government on clean growth will be consistent with broader government priorities, such as delivering clean air. All parts of the UK have a major role to play in delivering our ambitions on clean growth, and the Devolved Administrations have a range of plans and policies in place to deliver emission reductions. We will work closely with them, and with local leaders across the UK, as we develop the policies and proposals set out in this strategy.

The changes to our infrastructure and the pace of innovation will require significant investment from the private sector. The first steps to support the growth of the green finance sector in the UK are set out in this Strategy. We are building on a position of global leadership in finance and investment. These steps will be followed by ambitious policy proposals to further accelerate investments to deliver our Clean Growth Strategy. To help develop this longer-term work, the government has set up a new Green Finance Taskforce, comprising senior representatives from the finance industry and government.

3.2 Key policies and proposals

The key actions that this government will take as part of our strategy are set out below. While these policies and proposals will drive emissions down throughout the next decade, our focus is on the areas where we need to do more to achieve the fifth carbon budget through domestic action in the UK.

Through preparing this strategy, we have identified areas where we will need to see the greatest progress, both through technological breakthroughs and large-scale deployment, if we are to meet the fifth carbon budget through domestic action.

ACCELERATING

CLEAN GROWTH

1) Develop world leading Green Finance capabilities, including by:

*setting up a Green Finance Taskforce to provide recommendations for delivery of the public and private investment we need to meet our carbon budgets and maximise the UK’s share of the global green finance market

*working with the British Standards Institution to develop a set of voluntary green and sustainable finance management standards

*

providing up to £20 million to support a new clean technology early stage investment fund

*

working with mortgage lenders to develop green mortgage products that take account of the lower lending risk and enhanced repayment associated with more energy efficient properties

Improving business and industry efficiency – 25% of UK emissions

2) Develop a package of measures to support businesses to improve their energy productivity, by at least 20% by 2030, including by:

* following the outcome of the independent review of building regulations and fire safety, and subject to its conclusions, we intend to consult on improving the energy efficiency of new and existing commercial buildings

*

consulting on raising minimum standards of energy efficiency for rented commercial buildings

*

exploring how voluntary building standards can support improvements in the energy efficiency performance of business buildings, and how we can improve the provision of information and advice on energy efficiency to SMEs

*

simplifying the requirements for businesses to measure and report on energy use, to help them identify where they can cut bills

3) Establish an Industrial energy efficiency scheme to help large companies install measures to cut their energy use and bills

4) Publish joint industrial decarbonisation and energy efficiency action plans with 7 of the most energy intensive industrial sectors

5) Demonstrate international leadership in carbon capture usage and storage

(CCUS), by collaborating with our global partners and investing up to £100 million in leading edge CCUS and industrial innovation to drive down costs

6) Work in partnership with industry, through a new CCUS Council, to put us on a path to meet our ambition of having the option of deploying CCUS at scale in the UK, and to maximise its industrial opportunity

7) Develop our strategic approach to greenhouse gas removal technologies, building on the government’s programme of research and development and addressing the barriers to their long term deployment

8) Phase out the installation of high carbon forms of fossil fuel heating in new and existing businesses off the gas grid during the 2020s, starting with new build

9) Support the recycling of heat produced in industrial processes, to reduce business energy bills and benefit local communities

10) Innovation:

* invest around £162 million of public funds in research and innovation in Energy, Resource and Process efficiency, including up to £20 million to encourage switching to lower carbon fuels

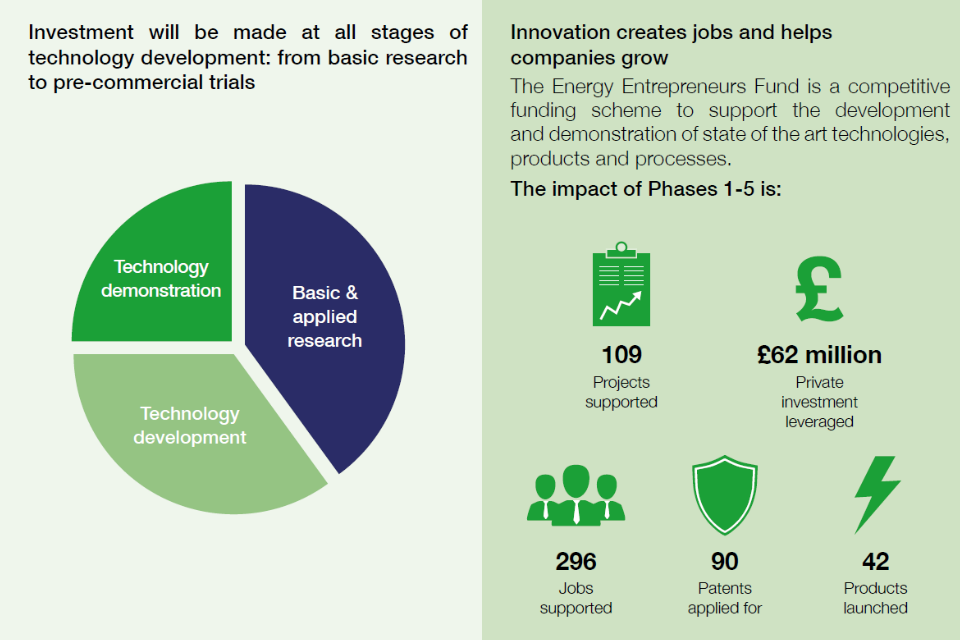

* support innovative energy technologies and processes with £14 million of further investment through the Energy Entrepreneurs Fund

* Improving our homes – 13% of UK emissions

IMPROVING

EFFICIENCY OF OUR HOMES

11) Support around £3.6 billion of investment to upgrade around a million homes through the Energy Company Obligation (ECO), and extend support for home energy efficiency improvements until 2028 at the current level of ECO funding

12) We want all fuel poor homes to be upgraded to Energy Performance Certificate

(EPC) Band C by 2030 and our aspiration is for as many homes as possible to be EPC Band C by 2035 where practical, cost-effective and affordable

13) Develop a long term trajectory to improve the energy performance standards of privately rented homes, with the aim of upgrading as many as possible to EPC Band C by 2030 where practical, cost-effective and affordable

14) Consult on how social housing can meet similar standards over this period

15) Following the outcome of the independent review of building regulations and fire safety, and subject to its conclusions, we intend to consult on strengthening energy performance standards for new and existing homes under building regulations, including

future-proofing new homes for low carbon heating systems

16) Offer all households the opportunity to have a smart meter to help them save energy by the end of 2020

Rolling out low carbon heating

17) Build and extend heat networks across the country, underpinned with public funding (allocated in the Spending Review 2015) out to 2021

18) Phase out the installation of high carbon fossil fuel heating in new and existing homes currently off the gas grid during the 2020s, starting with new homes

19) Improve standards on the 1.2 million new boilers installed every year in England and require installations of control devices to help people save energy

20) Invest in low carbon heating by reforming the Renewable Heat Incentive, spending £4.5 billion to support innovative low carbon heat technologies in homes and businesses between 2016 and 2021

21) Innovation: Invest around £184 million of public funds, including two new £10 million innovation programmes to develop new energy efficiency and heating technologies to enable lower cost low carbon homes

Accelerating the shift to low carbon transport – 24% of UK emissions

22) End the sale of new conventional petrol and diesel cars and vans by 2040

23) Spend £1 billion supporting the take-up of ultra low emission vehicles

(ULEV), including helping consumers to overcome the upfront cost of an electric car

24) Develop one of the best electric vehicle charging networks in the world by:

* investing an additional £80 million, alongside £15 million from Highways England, to support charging infrastructure deployment

*

taking new powers under the Automated and Electric Vehicles Bill, allowing the government to set requirements for the provision of charging points

25) Accelerate the uptake of low emission taxis and buses by:

* providing £50 million for the Plug-in Taxi programme, which gives taxi drivers up to £7,500 off the purchase price of a new ULEV taxi, alongside £14 million to support 10 local areas to deliver dedicated charge points for taxis

*

providing £100 million for a national programme of support for retrofitting and new low emission buses in England and Wales

26) Work with industry as they develop an Automotive Sector Deal to accelerate the transition to zero emission vehicles

27) Announce plans for the public sector to lead the way in transitioning to zero emissions vehicles

28) Invest £1.2 billion to make cycling and walking the natural choice for shorter journeys

29) Work to enable cost-effective options for shifting more freight from road to rail, including using low emission rail freight for deliveries into urban areas, with zero emission last mile deliveries

30) Position the UK at the forefront of research, development and demonstration of Connected and Autonomous Vehicle technologies, including through the establishment of the Centre for Connected and Autonomous Vehicles and investment of over £250 million, matched by industry

31) Innovation: Invest around £841 million of public funds in innovation in low carbon transport technology and fuels including:

ensuring the UK builds on its strengths and leads the world in the design, development and manufacture of electric batteries through investment of up to £246 million in the Faraday Challenge

delivering trials of Heavy Goods Vehicle (HGV) platoons, which could deliver significant fuel and emissions savings

Delivering Clean, Smart, Flexible Power – 21% of UK Emissions

32) Reduce power costs for households and businesses by:

* implementing the smart systems plan, which will help consumers to use energy more flexibly and could unlock savings of up to £40 billion to 2050

*

working with Ofgem and National Grid to create a more independent system operator to keep bills low through greater competition, coordination and innovation across the system

*

responding to the forthcoming independent review into the cost of energy led by Professor Dieter Helm CBE

*

publishing a draft bill to require Ofgem to impose a cap on standard variable and default tariffs across the whole market

33) Phase out the use of unabated coal to produce electricity by 2025

34) Deliver new nuclear power through Hinkley Point C and progress discussions with developers to secure a competitive price for future projects in the pipeline

35) Improve the route to market for renewable technologies such as offshore wind through:

up to £557 million for further Pot 2 Contract for Difference auctions, with the next one planned for spring 2019

working with industry as they develop an ambitious Sector Deal for offshore wind, which could result in 10 gigawatts of new capacity, with the opportunity for additional deployment if this is cost effective, built in the 2020s

36) Target a total carbon price in the power sector which will give businesses greater clarity on the total price they will pay for each tonne of emissions. Further details on carbon prices for the 2020s will be set out in the Autumn 2017 Budget

37) Innovation: Invest around £900 million of public funds, including around:

* £265 million in smart systems to reduce the cost of electricity storage, advance innovative demand response technologies and develop new ways of balancing the grid

* £460 million in nuclear to support work in areas including future nuclear fuels, new nuclear manufacturing techniques,

* recycling and reprocessing, and advanced reactor design

* £177 million to further reduce the cost of renewables, including innovation in offshore wind turbine blade technology and foundations

ENHANCING

THE BENEFITS & VALUES OF NATURAL RESOURCES – 15% of UK emissions

38) As we leave the EU, design a new system of future agricultural support to focus on delivering better environmental outcomes, including addressing climate change more directly

39) Establish a new network of forests in England including new woodland on farmland, and fund larger-scale woodland and forest creation, in support of our commitment to plant 11 million trees, and increase the amount of UK timber used in construction

40) Work towards our ambition for zero avoidable waste by 2050, maximising the value we extract from our resources, and minimising the negative environmental and carbon impacts associated with their extraction, use and disposal

41) Publish a new Resources and Waste Strategy to make the UK a world leader in terms of competitiveness, resource productivity and resource efficiency

42) Explore new and innovative ways to manage emissions from landfill

43) Support peatland through a £10 million capital grant scheme for peat restoration

44) Innovation: Invest £99 million in innovative technology and research for

agri-tech, land use, greenhouse gas removal technologies, waste and resource efficiency

Leading in the public sector – 2% of UK emissions

45) Agree tighter targets for 2020 for central government and actions to further reduce greenhouse gas emissions beyond this date

46) Introduce a voluntary public sector target of a 30% reduction in carbon emissions by 2020 to 2021 for the wider public sector

47) Provide £255 million of funding for energy efficiency improvements in England and help public bodies access sources of funding

Government leadership in driving clean growth

48) Work with businesses and civil society to introduce a ‘Green Great Britain’ week to promote clean growth

49) Reinstate a regular Clean Growth Inter-Ministerial Group responsible for monitoring the implementation of this Strategy and driving ambitious clean growth policies

50) Report annually on our performance in delivering GDP growth and reduced emissions through an ‘Emissions Intensity Ratio’

4. Investment in innovation for clean growth

To achieve the clean growth we want, the UK will need to nurture low carbon technologies, processes and systems that are as cheap as possible.

It is only through innovation that we will see new technologies developed and the cost of clean technologies come down.

5. TRACKING OUR PROGRESS

We want to deliver increased economic growth and reduced emissions. We have developed an Emissions Intensity Ratio

(EIR) to measure our clean growth performance which we will publish each year so we can track progress. To reach our 2032 targets we will need to drive the emissions intensity of the economy down by an average of 5% per year to 2032, an acceleration in the 4% annual fall since 199031.

The Emissions Intensity Ratio (EIR)

This measures the amount of greenhouse gases (tonnes of carbon dioxide equivalent) produced for each unit of Gross Domestic Product (GDP) created. Currently the EIR is 270 tonnes/£ million and it was 720 tonnes/£ million in 1990. By 2032, we expect the EIR will need to be nearly as low as 100 tonnes/£ million to meet our ambitions.

6.

NEXT STEPS

This strategy is not the end of the process. While this is an important milestone in our work to decarbonise the UK while growing our economy, our approach will develop and adapt to changing circumstances. We will update key elements of the strategy in line with our annual statutory responses to the Committee on Climate Change’s reports on progress, ahead of setting the sixth carbon budget by 30 June 2021.

We will also launch the following government consultations during 2017 and 2018 on:

* the design of a new industrial heat recovery programme

* making the private rented sector energy efficiency regulations more effective, and setting longer term

* energy performance standards across both the domestic private and social rented sectors

* a streamlined and more effective energy and carbon reporting framework for UK businesses to help them identify where they can cut bills

* a package of measures to support businesses to improve how productively they use energy

our strategic approach to the aviation sector in a series of consultations over the next 18 months

A full list of the actions and milestones arising from this strategy is set out at Annex B. Many of the future actions the government will be taking, expanding on the proposals above, will be set out in the 25 Year Environment Plan, which will be designed to be a sister document to this Strategy, and in a long term strategy for the UK’s transition to zero road vehicle emissions. Taken together, these set out the government’s approach to fulfilling its commitment to leave the environment in a better state than it inherited. Along with the Industrial Strategy White Paper, to be published later in 2017, these will form a critical part of our future progress.

The government cannot achieve the changes needed to our economy by itself. Outside action on public sector emissions, the government’s key role is to set the framework for action across the economy. Beyond that, clean growth has to be a shared endeavour between government, business, civil society and the British people. Creating this supportive environment will help attract the domestic and international investment the UK wants. Therefore from 2018 we will work with private partners and NGOs to introduce a Green Great Britain Week.

6.1 Green Great Britain Week

An annual event to:

* focus on climate and air quality issues across the UK

* demonstrate our progress and successes on climate action

* share the latest climate science

* highlight and promote economic opportunities arising from clean growth especially to international investors

7. FEEDBACK

We welcome views and comments on our approach and these should be sent to CleanGrowthStrategy@beis.gov.uk by 31 December 2017. Views received in response to both this strategy and the detailed policy proposals which will follow it, will be considered as we update key elements of our strategy before setting the sixth carbon budget by 30 June 2021.

8.

END NOTES

COP

THAT - The United Nations Climate Change Conferences are

yearly conferences held in the framework of the United Nations

Framework Convention on Climate Change (UNFCCC). They serve as

the formal meeting of the UNFCCC Parties (Conference of the

Parties, COP) to assess progress in dealing with climate

change, and beginning in the mid-1990s, to negotiate the

Kyoto Protocol

to establish legally binding obligations for developed

countries to reduce their greenhouse gas emissions.

1995 COP

1,

BERLIN, GERMANY

1996 COP

2, GENEVA, SWITZERLAND

1997 COP

3, KYOTO, JAPAN

1998 COP

4, BUENOS AIRES, ARGENTINA

1999 COP

5, BONN, GERMANY

2000:COP

6, THE HAGUE, NETHERLANDS

2001 COP

7, MARRAKECH, MOROCCO

2002 COP

8, NEW DELHI, INDIA

2003 COP

9, MILAN, ITALY

2004 COP

10, BUENOS AIRES, ARGENTINA

2005 COP

11/CMP 1, MONTREAL, CANADA

2006 COP

12/CMP 2, NAIROBI, KENYA

2007 COP

13/CMP 3, BALI, INDONESIA

2008 COP

14/CMP 4, POZNAN, POLAND

2009

COP 15/CMP 5, COPENHAGEN, DENMARK

2010 COP

16/CMP 6, CANCUN, MEXICO

2011 COP

17/CMP 7, DURBAN, SOUTH AFRICA

2012 COP

18/CMP 8, DOHA, QATAR

2013 COP

19/CMP 9, WARSAW, POLAND

2014 COP

20/CMP 10, LIMA, PERU

2015 COP

21/CMP 11, PARIS, FRANCE

2016 COP

22/CMP 12/CMA 1, MARRAKECH, MOROCCO

2017 COP

23/CMP 13/CMA 2, BONN, GERMANY

2018 COP

24/CMP 14/CMA 3, KATOWICE, POLAND

2019 COP 25/CMP 15/CMA 4 TBA

LINKS

& REFERENCE

https://www.gov.uk/government/publications/clean-growth-strategy/clean-growth-strategy-executive-summary

https://www.theccc.org.uk/

MARINE

LIFE - This humpback whale is one example of a magnificent

animal that is at the mercy of human

activity on planet earth

such as climate change. Humans are for the most part unaware of the harm their fast-lane

lifestyles are causing. We aim to change that by doing all we

can to promote ocean literacy and climate awareness.

This

website is provided on a free basis as a public information

service. Copyright © Cleaner

Oceans Foundation Ltd (COFL) (Company No: 4674774)

2018. Solar

Studios, BN271RF, United Kingdom.

COFL

is a charity without share capital.

|